Pipe breaks can happen in an instant. A clog in your pipe becomes a complete block and as water pushes against it, your pipe bursts, resulting in significant water damage to your home. After turning off the water and drying out your home, you discover your ruined carpets. Who’s paying for this? Does your homeowners insurance cover broken pipes in Florida? The answer varies from policy to policy.

Many Florida insurance policies cover water damage. However, in many cases, it comes down to how the damage occurred. Most policies will cover a pipe break if it’s unforeseen, such as a burst pipe, an air conditioner that suddenly releases all its water, or an accident with your washing machine.

The Cliff Notes: Key Takeaways From This Post

- 1Insurance companies tend to regard the slow, leaky damages from pipe breaks as something homeowners should have taken care of before it became a serious issue.

- 2Most insurance policies cover resulting damage from unexpected events- such as gushing water that follows broken or burst pipes- but not initial damage.

- 3To prevent a denied claim, homeowners should keep records of plumbing inspections and repairs and make sure all pipes are in good working order.

- 4If the insurance company denies a claim for valid damage, consumers can get a second opinion from an organization or lawyer experienced with insurance rules in their area.

Pipe Breaks Cause Different Types of Water Damage

There are two types of water damage that can result from pipe breaks. There is sudden and unexpected damage, such as a burst pipe behind a wall in your bathroom or a slow, leaky pipe under your sink. In most cases, your Florida homeowners insurance policy will cover the sudden and unexpected damage but not the slow, leaky kind.

Insurance providers in Florida tend to view the slow, leaky kind of damage as something you should have taken care of long before it became a serious issue. This is why it can be tricky to determine if homeowners insurance covers pipes and plumbing at all.

Here’s another way to look at it. Your HVAC system is one of the most expensive appliances in your home, and you expect it to last around 20 years. When the time comes to replace it, you wouldn’t file a property insurance claim, because it’s part of the cost of owning and maintaining a home.

Now, let’s say, you replaced your HVAC system two years ago, and a huge hail storm batters it into little pieces. Under these circumstances, you’d expect your insurance to cover the costs of replacement, and they would.

Problems and damages that are caused by normal wear and tear and/or gradual damage are more than likely aren’t covered by insurance. Of course, if you have exacerbated the damage due to “resulting damage” from an unexpected event, then insurance would cover it.

For example, your water tank gets a crack and breaks open, your washing machine opens up, or a pipe bursts, spilling water over the floor that already had minimal damage, then insurance would cover it.

How Many Insurance Companies Regard Pipe Breaks

Most insurance companies regard your home’s plumbing as general maintenance and your responsibility. As the property owner, it’s your job to tighten screws, allow water to drip on cold nights to avoid frozen pipes, and remove any clogs as soon as possible. You do these things to keep the pipes in good condition and maintain your property value.

You also need to make sure that you’re getting rid of mold and mildew, which can be a sign of a small crack in your pipes. If you suspect, you have a hairline fracture, the insurance company holds you responsible for fixing the issue.

The hairline cracks and leaks cause damage over a period of time. Insurance companies consider this gradual damage as something avoidable, and they normally won’t cover the damages. However, there’s a big difference between a slow leak and a burst pipe.

We’ve all heard the story about a friend of a friend who comes home from vacation to find the lower floor of their home has become a swimming pool due to a burst pipe. It’s one of the most frightening urban legends for a homeowner, but on the positive side, your insurance company will more than likely cover the cost of the damages.

Gushing water that’s almost impossible to control follows broken or burst pipes. It’s also going to create significant damage very quickly. Homeowners insurance typically covers the destruction and damage caused by gushing water. The clause in your policy that covers this damage is the all-perils section. You can look for it in your own insurance policy paperwork.

In order for the insurance to cover a claim, the damage must occur suddenly and by accident. It won’t be covered if the damage was easily preventable by you or regular maintenance.

As an example, imagine you live in a colder section of the country, and your electricity is out due to non-payment. In subfreezing temperatures, your pipes freeze and burst. If you’d had electricity, this might not have happened. Your insurance company is going to consider this negligence and won’t pay the claim.

Even though insurance policies usually exclude wear and tear, the policies usually cover damage that results from the wear and tear. What this looks like in real life is that the insurance company might be able to avoid paying to fix the pipe that supplies water to your sink when it wears out, but has to pay for all the water damage that resulted when the worn-out pipe causes your house to flood (or in insurance language, caused an “ensuing loss”).

What Damage Do Most Homeowners Policies Cover?

Insurance companies tend to break damage into a few categories, including resulting damage and initial damage. The resulting damage is damage that is a result of a catastrophic event, such as a ruined carpet due to a burst pipe. Initial damage is the first damaged thing, so the pipe breaking would be the initial damage.

Check your insurance policy. If the wording on the policy says that resulting damage due to something such as a broken pipe or exploded appliance is eligible for repayment, then you can expect them to cover the damages. This would include damage to carpets, furnishings, floors, paint, drywall, and more. It can also include the expense of drying out the home and taking the necessary steps to avoid mold and mildew from the water damage.

If only the resulting damage is covered under your policy, the policy doesn’t cover the cost of replacing your pipes, because it’s initial damage. However, the policy covers the vast majority of damage and destruction.

Tips to Avoid a Denied Water Damage Claim

As a homeowner, you know that your home needs routine maintenance. As part of that maintenance, it’s a good idea to routinely have your plumbing inspected, and you need to keep the records of the plumber visits in case of a future insurance claim. Along with inspection records, you need to keep a record of all repairs as well as the different professionals who inspect your plumbing.

All the pipes in your home lack the same service life. It’s beneficial to replace the pipes when they reach their maximum lifespan to protect your property and the ability to successfully file a water damage insurance claim. During the winter months and cold snaps, you need to ensure your home’s heat is running. If you go out of town for a few days or an extended vacation, you need to keep the heat on, even if it’s set lower than it would be if you were at home to protect your pipes.

Somewhere in your home or on your property is the master water shut-off valve. In case of an emergency, you use this valve to immediately stop the flow of water into your home. You need to make sure that you and other members of your family know the location of the valve and how to use it. You need to routinely check the valve and ensure it’s in good working order.

It’s up to you to do everything that you can to avoid the appearance of negligence. Keeping up with routine maintenance and organizing your paper trail will go a long way to ensure your insurance coverage.

Insurance Claim Denied? Now, What Do You Do?

It happens. You file your claim, the inspector comes to your home, and the insurance company denies the claim. Now, what do you do?

If you think your claim is valid, but the insurance company denied the claim, you should hire a professional plumber for a second opinion. You can contact a consumer advocacy organization if the professional agrees with you. It’s a good idea to find an organization that’s familiar with the insurance rules in your area. You also have the option of hiring a law firm to protect your interests.

With your denial, there may be information on appealing the claim. You should definitely take these steps for an appeal. You can also contact your state’s insurance commissioner and file a complaint.

Whatever you decide to do, you should act quickly to protect your rights. The more time that passes means the fewer rights and options that you have available to you.

Contact Our Firm for a Free Insurance Policy Review

If you aren’t sure if your homeowners policy covers pipe breaks, you need to schedule an appointment with your broker or agent to discuss your coverage. When talking to your agent, make sure that you don’t focus on only covered items. You need to discuss what situations the policy excludes too. You don’t want any surprises.

It’s a good idea to have a comfortable grasp on what your policy covers and what it doesn’t. It’s also beneficial to make small repairs to avoid larger issues at a later date.

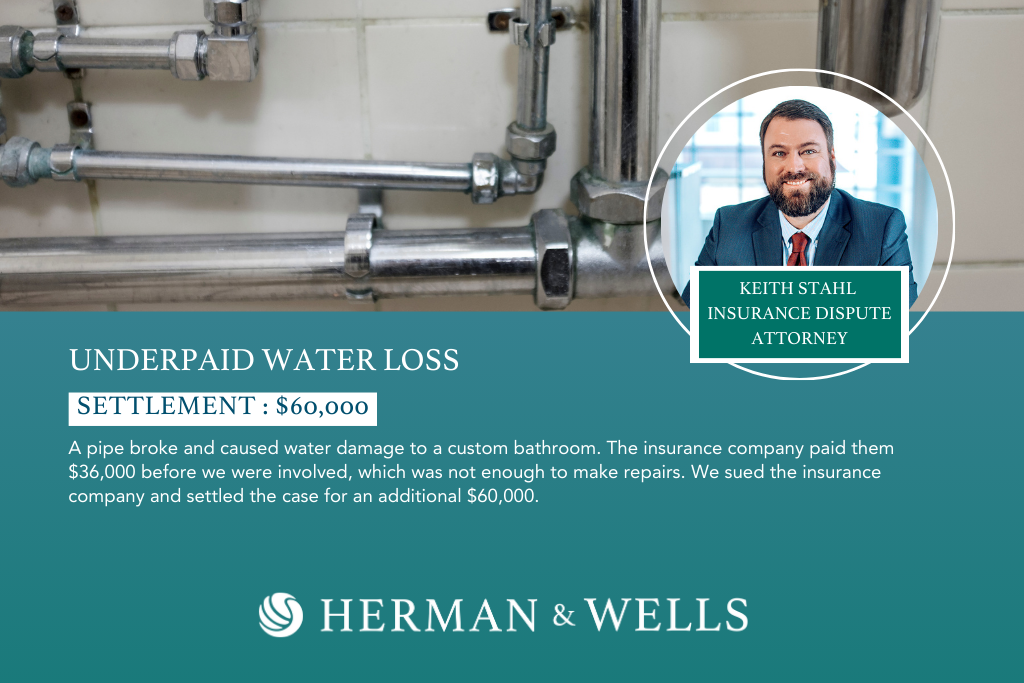

At Herman Wells, we understand the ins and outs of the insurance game. We’re ready to help you with a claim from burst pipes. Contact our law firm for a free consultation or policy review.