Table Of Contents

Is your insurance company refusing to cover your water damage insurance claim? Unfortunately, this is a serious situation that many Florida homeowners find themselves in each year. In fact, according to recent reports, nearly half of all water damage claims are denied. But don’t give up just yet. You have the right to dispute your insurance company’s decision. To start, you should contact one of our water damage insurance lawyers in Florida ASAP.

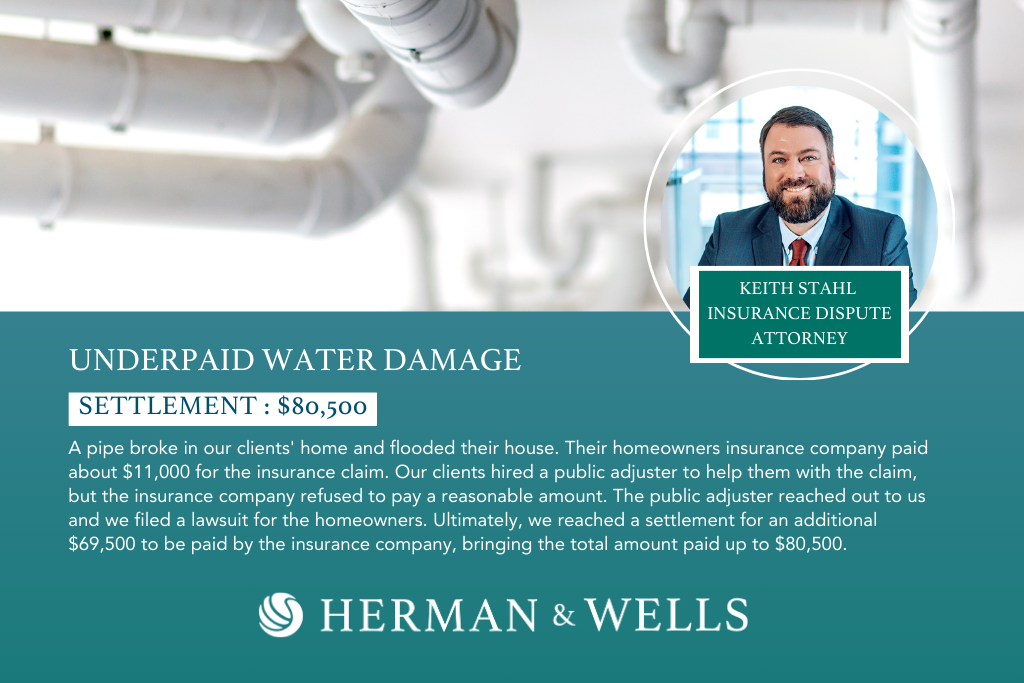

Our insurance dispute attorneys have years of experience advocating for policyholders in court against the biggest insurance companies in Florida. We know how to get them to pay for what they owe. So if you’ve been denied a water damage claim, contact us today for a free, no-obligation evaluation. We’ll review your claim and let you know what your next steps should be.

Call (727) 821-3195 if you’d like to speak with one of our Florida water damage insurance lawyers immediately. During this initial evaluation, our seasoned insurance dispute attorneys will review your insurance claim for free. Our law firm’s main offices are in Pinellas Park, but we have attorneys in St. Petersburg, Tampa, Seminole, Dunedin, Palm Harbor, Lakewood Ranch, Bradenton, and Sarasota.

Water damage can be a costly and devastating event for homeowners, and the type of water damage that is covered by a standard homeowner’s insurance policy can vary. Some homeowners may be surprised to learn that their policy does not cover all types of water damage. Let’s kick things off by reviewing what types of water damage are typically covered by homeowners’ insurance policies.

Homeowner’s insurance policies typically cover water damage caused by sudden and accidental events, such as burst pipes or overflowing washing machines. However, most policies exclude coverage for water damage that is caused by gradual events, such as leaks. In addition, most policies limit the amount of coverage available for water damage.

While every policy is different, most homeowners’ insurance policies will provide some coverage for water damage. If you are unsure about what your policy covers, you should contact your insurance agent or company to get clarification on what type of water damage coverage your policy offers.

There are a few common water damage insurance policy exclusions that you should be aware of. One is that damage caused by natural disasters, like hurricanes or tornados, is typically not covered. Another is that damage caused by floods is not usually covered, although there are some exceptions. And finally, most policies do not cover damage caused by seepage or leakage. So if you’re concerned about any of these types of damages, it’s important to check with your insurance company to see if they’re covered under your policy.

Florida is well known for its hurricanes and severe storms. These weather conditions often lead to water damage in homes and businesses. In order to protect property owners, many insurance companies offer water damage insurance as part of their policies. The most common causes of water damage insurance claims in Florida are:

If your home or business has been damaged by water, it is important to contact your insurance company as soon as possible. They will be able to help you determine if you have coverage and what steps need to be taken in order to file a claim. Call a Florida water damage insurance attorney for more information.

When it comes to filing a water damage insurance claim, it’s important to be aware of the different types of damage that can occur. One type of damage that can be tricky to deal with is gradual water damage. This type of damage can be hard to spot and may not be covered by your insurance policy.

If you’re dealing with a water damage insurance claim and you think you may have suffered from gradual damage, it’s important to speak to an insurance dispute lawyer. They will be able to help you understand your policy and determine if you’re eligible for compensation.

There are several common causes of gradual damage that might prevent you from receiving compensation:

It’s possible that you don’t know why your claim was rejected. However, if you attempted to submit a claim and it turned out the damage was gradual, this is most likely why you were denied.

If you detect water damage in your Florida home, you should take the following steps:

If you detect water damage in your Florida home, the first thing you should do is shut off the water. This will help minimize the damage that is caused by the water and will also help prevent further damage from occurring.

If there is any water damage to your plumbing, it’s best to call a plumber to take a look at it. They will be able to fix any leaks or broken pipes and will help prevent further damage from occurring.

Once you have taken care of the immediate issues, you should contact your insurance company right away. They will be able to help you file a claim and will start the process of getting your home back to its original condition.

If you are a Florida resident and have suffered water damage to your property, you may be wondering what to do next. Filing a claim with your insurance company is the first step, and our experienced Florida insurance lawyers can help make the process as smooth as possible. Here are some tips to keep in mind when filing a water damage insurance claim in Florida.

First, it is important to document the damage as thoroughly as possible. Take photos or videos of the damage, and make a list of all the items that were affected. This will help support your claim when you file with your insurance company. Second, be sure to contact your insurance company as soon as possible after the damage occurs. They may have specific procedures you need to follow in order to file a claim properly. Don’t wait until it’s too late – act quickly and consult with an expert if needed!

Third, be prepared to negotiate with your insurance company. They may try to lowball you on the compensation you deserve, but our experienced Florida water damage insurance lawyers will fight for what you are entitled to. Finally, don’t forget that you have rights. If your insurance company is giving you the runaround or denying your claim altogether, contact a Florida water damage insurance lawyer. A lawyer can help protect your rights and get you the compensation you need to recover from this difficult situation.

Did you know that insurance companies in Florida routinely deny water damage claims? In fact, a recent study showed that nearly 60% of all water damage insurance claims are denied. There are a number of reasons for this, but some of the most common ones are:

In Florida, insurance companies are required to have a claims process in place that allows policyholders to file a claim within a certain amount of time after the damage occurs. If the policyholder fails to file a claim within this time frame, the insurance company is likely to deny the claim.

For example, a hurricane might cause water damage to a home, but this type of damage is not typically covered under a standard homeowners insurance policy. If the damage is caused by an act of nature, the insurance company is likely to deny the claim.

In some cases, the damages caused by water damage are not covered by the policyholder’s insurance. This might be because the policy does not cover this type of damage, or because the policy does not cover the full amount of the damages. If the policyholder does not have sufficient coverage to cover the damages, the insurance company is likely to deny the claim.

In some cases, the insurance company may deny a water damage claim if the policyholder has filed multiple claims in a short period of time. This is because the insurance company may view the policyholder as being too risky or not worthy of coverage. If the policyholder has filed multiple claims in a short period of time, the insurance company is likely to deny the claim.

If you have experienced water damage in Florida and your insurance claim has been denied or underpaid, you may be wondering what your next steps should be. Thankfully, there are a number of steps you can take to dispute a denied or underpaid insurance claim.

The first step is to reach out to your insurance company and explain the situation. If you are not satisfied with their response, you can then reach out to a water damage insurance lawyer who can help you file a formal complaint. Additionally, you can file a complaint with the Florida Department of Financial Services. By taking these steps, you can increase your chances of getting the compensation you deserve for your water damage.

Water damage can be extremely costly to repair. If you have experienced water damage in Florida, do not hesitate to reach out to a Florida water damage insurance lawyer for help. They can guide you through the process of filing a formal complaint and help you get the compensation you deserve.

If your insurance claim has been denied or underpaid, it is worth getting a second opinion from an attorney with experience advocating for policyholders in court. Our insurance dispute attorneys can guide you through the process of filing a formal complaint and ensure that you get the compensation you deserve. If your Florida home has suffered water damage that should be covered by your insurance company, call (727) 821-3195 to request a free claim review. The water damage insurance lawyers at Herman & Wells are ready to help you and your family.